I apologise, it’s been a while. I’ve been busy recently, plus this writeup has taken me longer than many others. As any readers would know, I have a passionate interest in short selling. So far I’ve kept my writeups to business shorts with what I perceive to be operational issues, however I believe I’ve stumbled across a borderline fraudulent blatant stock promote. Not only that, I haven’t seen any other coverage of this company on the short side, with it being too small for most firms to look at shorting. With that all out of the way I would like to introduce you to the subject of today's writeup: Nuvve Holdings.

The Business

Nuvve is an electric vehicle company that supplies electric buses and vehicle to grid chargers with their proprietary software. Currently their main customer base is American schools taking advantage of various rebates to purchase this technology at significantly discounted prices. Vehicle to grid (V2G) technology involves using two way charging stations to utilise electric vehicles as batteries and essentially supply energy back to the grid when in peak hours and not in use, while charging when off peak hours. In theory, at scale this has the potential to significantly ease strains on the electrical grid as vehicles can charge during times when the grid load is low, while supplying the grid with power while the grid load is high.

V2G Tech

While many tout V2G as the solution to our energy problems there are many issues with widespread adoption, and the research is mixed at best especially for current utility. Regarding V2G, Elon Musk has stated it “has much lower utility than people think”[1], while Chargepoint (which has almost 30 times the R&D budget of Nuvve) has stated “V2G is not currently ready for widespread use”[2]. Furthermore, V2G is only useful with standardised vehicles (most current EVs don’t offer it) meaning it’s most viable for fleet sales[3]. Finally, it is only useful with significant periods of downtime in peak electricity hours, ruling out vehicles that have to be driven regularly[4]. With this all considered it makes sense why Nuvve has focused its effort on the school bus market, where V2G makes the most sense. However, their $176B tam is incredibly unrealistic, with postal fleets (15%) and public transit (20%) being uneconomical due to their constant usage demand. Furthermore, they’re clearly losing out on market share already as I’ll discuss later, with competitors Blue-Bird and Proterra doing many multiples of revenue compared to them.

More importantly however, the company markets itself as an electric vehicle and charging technology company, when in reality it’s just a distributor. While they aren’t secretive about their buses being from Blue-Bird corporation, they don’t bring much attention to their charging stations. While they regularly refer to their chargers as “our technology” in presentations, they are actually sourced from Rhombus Energy Solutions and rebranded, a name that shows up only once in their annual report and not at all in their quarterly. With little of their revenue coming from services, I believe the company is being deliberately misleading and overpromotional to investors who mostly believe they are investing in a charging technology company.

Their point of difference is their “intelligent energy platform”, which manages the bidirectional charging for big fleets. I don’t believe this to be a real point of difference as every charging company has software for dynamic load management that could very easily be adapted for V2G, all of whom have significantly more funds and scale than Nuvve. Many of their competitors have R&D budgets magnitudes larger and yet choose not to invest in developing this technology, suggesting it’s either uneconomical or unviable.

Thanks for reading Questionable Investment Thoughts! Subscribe for free to receive new posts and support my work.

So how do they get any sales at all? The market for electric school buses is incredibly heavily subsidised both on the federal level and more locally. In interviews with customers, the customers claim to be essentially getting the fleet upgrades for free[4]. This means that some of Nuvve’s customers are price insensitive as they aren’t actually paying for the vehicles and chargers themselves most of the time.

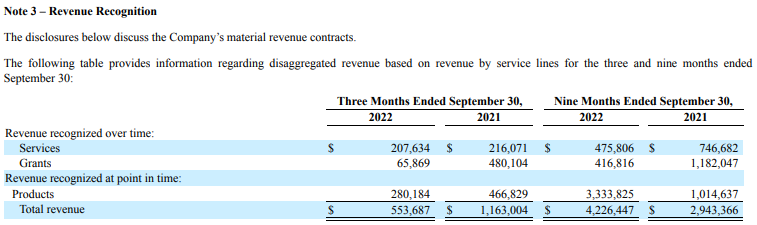

With all this considered, it’s no surprise their financials are atrocious. Even compared to other electric vehicle companies Nuvve stands out for how little money they make with their trailing 12 month revenue being a measly $5m compared to Proterra and Chargepoint (direct competitors in electric buses and charging) making $300m and $376m in revenue respectively. The fact is that there is currently huge demand for electric vehicles, especially in the bus fleet space however it’s clear that they just aren’t capturing any of it. This results in a negative operating cash flow of around $30m annually, a ridiculous -600% cash flow margin.

In spite of this, their CEO, COO and CFO gave themselves a combined $2.4M in compensation last year (not including non exercisable options), 54% of total revenue. Meanwhile, directors pocketed another $1.25m between the 5 of them. I believe this to be a management enrichment scheme with essentially no product and no realistic path to any sort of profitability. In spite of all these issues, management has been incredibly promotional. They have taken any opportunity to pitch, even going onto interviews with small youtube channels in order to gather new bagholders for their company. Management have taken advantage of the EV boom to take 100’s of millions of dollars from shareholders and funnel them into insiders pockets while returning no value of any kind.

Nuvve was the beneficiary of the huge January frenzy, gaining 400% in a month. At the peak of this the company announced that they were doing a highly dilutive capital raise for $25m at a market cap of $50m. Since then the stock has crashed 50% to a market cap of $26m. I’m unsure how much of the offering they were actually able to sell and at what prices, and therefore unsure how well capitalised they are going forward. A week after this, in a feeble attempt to pump the stock again the company announced an investigation into illegal short selling of their stock. At a short interest of 5% according to Tikr, and no public short reports before the release of this, this is an obvious ploy to try and pump the stock back up suggesting their raise possibly didn’t do as well as they hoped. In spite of the share price decline and uncertainty around cash position I still believe this to be a viable short as they still only have max a year of cash runway left. At a 10% borrow, it’s certainly shortable for a personal account or a larger account shorting quantitatively.

I just wanted to add a few other red flags I found looking into it. Nuvve was brought to market in a SPAC deal sponsored by Neogenesis Holding Co. This seems to be the only major deal this firm has made, and I can’t find any other information on this sponsor online anywhere. The CEO and CFO of Newborn (the acquisition corp) are Wenhui Xiong and Jianjun Nie have both come from a firm called shanghai Jiusongshanhe Equity[6]. Again I can’t seem to find any information about either man or the firm. While none of this is evidence towards any wrongdoing, they are just more red flags on a company already covered in them.

Add to this, their subsidiaries seem to have very few operations. When their French subsidiary was disbanded in 2019 it only had 2 employees. A look at their European subsidiary Dreev’s website shows it to be tragically bare, with operations slated to start in 2024 despite being around for 4 years already. Levo, their joint venture financing and fleet-as-a-service subsidiary has a similarly bare website, has been consistently loss making and only shows 6 employees on LinkedIn (of which 2 are directors from the partner firms). The joint venture involved financing pledges from Stonepeak Asset Management and Evolve Transition Infrastructure for up to $750m however so far only $5m of that has been used. This joint venture raises major red flags for me with a complicated capital structure composed of multiple layers of warrants, common and preferred shares. Furthermore, Stonepeak created a whole new subsidiary seemingly (as far as I could tell) for the sole purpose of this investment called Stonepeak Rocket Holdings LP. Meanwhile, Evolve is a very strange, overleveraged gas royalties company which has also been consistently unprofitable and is owned 88% by the aforementioned Stonepeak. Evolve is down 99.9% all time, 97% in the last 5 years and 80% from its peak during the February 2021 meme squeeze. While again I’m not alleging anything specific here, the complexity and strangeness of this jv raises significant red flags for me.

So to sum this all up the Nuvve is promoting itself as an electric vehicle technology company when in reality they are distributing other people’s chargers and vehicles and slapping some generic software over the top. Management have clearly no regard for shareholders and have taken any opportunity to fleece shareholders of capital. Even if their market opportunity is as viable as they say it is, with minimal revenues it’s clearly apparent that they aren’t capturing any of it. Add on to this the company has a shady history with red flags around every element of the business. At best it’s a shameless stock promotion, at worst it’s a fraud.

Obviously full disclosure I have a small short position in Nuvve. Nuvve is only really suitable for either a personal account or a quant portfolio with only $300000 worth of shares available to borrow on IBKR. This report is more just a practice and demonstration of my skills, along with exposing a company and management team I believe to be deeply unethical. Any feedback, criticisms or questions would be very welcome, as always I’m just looking to improve.