Today I’m going to pitch you two ideas. On one hand we have an overlevered shitco being pumped by a dodgy investment bank on the short side. On the other hand we have a cheap bond with a 10% yield, trading 30% below par, backed by significant tangible book value maturing in a year. Both securities are actually tied to the same company, and I believe set up a very attractive return profile for Fossil Group $FOSL/$FOSLL from a long short perspective.

Fossil Group, Inc. is a global watch seller selling under both their own brands like Fossil and Skagen, and licensed brands such as Michael Kors and Emporio Armani. They distribute products worldwide through wholesale, retail stores, and e-commerce. Fossil has been steadily declining since its peak in the early 2010’s and, with the exception of the 2021 retail boom, have had 5 straight years of unprofitability. The watch market has been very weak since 2021 and the company sits at an awkward, mid range ”affordable luxury” price point for most of their brands, lacking the pricing power of their luxury counterparts. The company is now in an aggressive restructuring, closing underperforming stores and focusing on their core brands (after a disastrous foray into smartwatches and wearables). The company and their brands have terrible ratings on websites like Trustpilot and Productreview, with a detailed review describing their watches as “more than disappointing”.

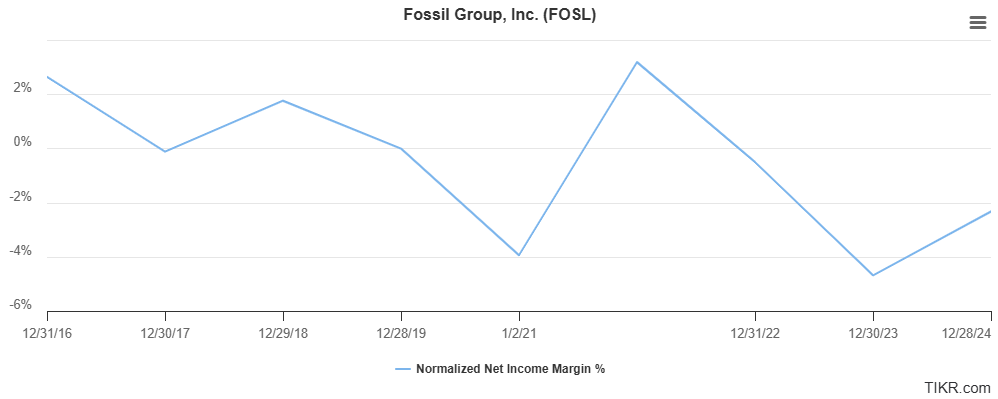

The turnaround does seem to be somewhat working, bringing operating margins from -6.5% in 2023 to -.5% in the last 12 months while revenue has fallen 20%. Unfortunately, while the company is borderline break even on EBIT, they have $18m of interest payments a year (against -$6m operating income) due to $185m of debt and income tax payable. The debt is particularly concerning as it’s due in November 2026. With only $80m of cash available it’s hard to see how they pay off the debt without a dilutive capital raise or a refinancing (which would be tricky as they continue to lose money and are probably paying below market interest on their current bonds).

A notable thing here is the involvement of Maxim Group, a small, B-Riley-esque investment bank that put out a target price for the stock recently. I make the B-Riley comparison because Maxim similarly has a focus on small cap shitcos and similarly has put out some frankly ridiculous recommendations and price targets. At the time of writing Fossil Group is up 27% in a week after Maxim put out a $5 price target on the company (currently $1.6). Having read through the report I see nothing that justifies that target, and with analyst Tom Forte holding similarly high targets for scams and shitcos like $BOXD, $RUM, $RZLV and $BIRD it doesn’t worry me. However I do think that it has provided us with a great short setup, with the company up alot on a nonsense price target with low liquidity. Additionally, Maxim has a history of putting out inflated price targets for companies it later does capital raises for, which as we look at later would be a positive for the thesis.

I believe that this situation provides us with a fantastic, low risk long short opportunity. Currently the bonds trade at a 30% discount to par and a 10% yield, while the common continues to be unprofitable. As far as the potential returns, there are a variety of different outcomes here I want to look at.

The first outcome is that the turnaround doesn’t work, results fall off the equity is zeroed. In this scenario the trade likely performs decently as the short pays out 100% (with .3% cost to borrow) and any recovery on the debt is just profit. With $480m of current assets ($182m of inventory) against $270m of liabilities (ex the 26 notes) there should be plenty available even in a worst case scenario.

The second outcome is an impairment of the equity with the debt being fully paid out. Unless we see a miraculous recovery in sales growth over the next year I think this is the most likely outcome, as the company continues around breakeven but is forced to raise capital to pay off the debt. This would likely result in poor performance for the stock (-20% to -50%) while seeing the debt paid out in full (+60%) and would be pretty much the ideal outcome here. What’s interesting is that even in the silly bull case from Maxim, they still assumed a very weak FY25 and a capital raising to pay off the debt.

The last outcome is that the turnaround is successful, with the debt being paid off and the company recovering to profitability. I crunch some very rough numbers to see what that could look like. When the company was profitable historically it sat around low single digit margins so let's imagine a world where they return to profitability and they manage 4% operating margins. In this world we are probably looking at around $40m unlevered fcf against a current enterprise value of $320m or an 8x multiple. I’m using EV and unlevered FCF here as I think a capital raise is likely here, so I think this is probably the simplest way to look at things. My point here is that even in a potential recovery the company isn’t screamingly cheap, and more importantly we have a 60% buffer through the debt, which would be paid out in full. Obviously post recapitalisation the multiple may be higher or their post recovery operating margins might be higher, but I think the likelihood of this strong of a turnaround is low and we have a nice margin of safety through the upside in the debt.

I think most of the risks here are pretty straightforward. Risks to the downside are limited, as any zeroing of the debt would also see a zeroing of the equity. The only issue would be in some sort of transaction that forced the debt further down the capital structure, but I don’t see how that would happen. To the upside there’s short term price risk as markets are irrational and this is a low volume small cap shitco that could do anything. However, with the 2026 bonds I do believe Fossil has an overhang that will limit irrational upward price movements, aided by the lack of “memeability”. Finally, the biggest risk to the stock is a genuinely successful turnaround. With regards to this, management’s own estimates have them unprofitable with sales declining for FY25. Any signs of improvement will come in 2026, and to be honest after a decade of failed turning around I simply don’t see enough changing to make a significant positive improvement.

With my newfound Survivor money I’ve been thinking a lot about finding good, uncorrelated bets to diversify my portfolio. The Fossil Group long short idea is a trade that likely outperforms in a down market. However, unlike most generic shorts, Fossil doesn’t move with the frauds and scams and more importantly has a margin of safety through the positive performance of the bond, along with very good performance if the stock remains flat. I believe this idea offers a nice return over a year and a half for fairly low risk and I currently hold a 3% position.

Nice find

Good stuff mate.