Focusing on Focus Point

This is going to be a shorter writeup than many of my others, as this is as simple and clean an investment case as you can get. It’s not often that you get a company with low cyclicality, in a dominant competitive position, with a decade of clean, consistent growth at a sub 10x PE ratio, however in the small caps of Malaysia that’s what I believe we’ve found in Focus Point Holdings Berhad ($FOCUSP), Malaysia’s largest optical retailer.

The Business

Focus Point runs 200 glasses stores across Malaysia, making up around 20% of the market. The Malaysian optical retail market is highly fragmented, being mostly made up of local mom and pop operators. Focus Point has been steadily taking share for the last 3 decades as the low cost franchise option, expanding by establishing new stores themselves, partnering with franchisees and converting existing optical stores into franchisees. Focus Point is well positioned to continue to grow their store count as they have a clear competitive edge on the operators that make up most of the other 80% of the market. For 2025 they opened 10 new stores, running at about 5% annual store growth. Their target for 2026 is 15 new self operated stores, plus 5 new franchises, which would be around 10% store growth.

This idea particularly attracts me due to the non-cyclicality. The core optical business is about as non-cyclical as it gets. Prescriptions expire, glasses break, 20% of their revenue comes from contacts, a recurring, non discretionary consumable. This is borne out in the 2020 numbers which saw earnings only down 25% in spite of their physical stores being forcibly closed. 21 and 22 then saw a rapid rebound as people’s deferred eyewear purchases returned. Additionally, revenue per store has been steadily increasing as they expand their corporate sales (employer optical benefits) and premiumisation of the product mix improves.

The only notable hair on the thesis here is their F&B business Komugi bakery. In 2012 the company bizarrely decided to expand into the F&B business with a Japanese bakery store. Komugi has never been a meaningful profit driver for the company despite contributing 15% of company revenue. Profitability has been inconsistent and after 3 years of small profits, contributed an MYR $3m loss in 2025. Q1 2026 was stronger with the segment breaking even due to cost cutting, but this segment is low quality, low margin and exposed to economic cyclicality in a way the core business isn’t and has the potential to be a drag on company earnings.

Management and ownership are pretty standard here for a family run business. The company was founded by current CEO Dato’ Liaw Choon Liang, and his family collectively owns 51%. Capital allocation has been almost flawless, with their move into F&B the only blemish on their record. Other than that there’s been no silly acquisitions, no empire building, no cash hoarding, just a consistent dividend along with smart, steady reinvestment in the business. Remuneration is reasonable, and I haven’t seen any red flags that would lead to me doubting their ability to continue to run the business. Instead we have a well incentivised founder with the majority of his family wealth behind the business he has built from scratch.

Founder Dato’ Liaw

The Financials

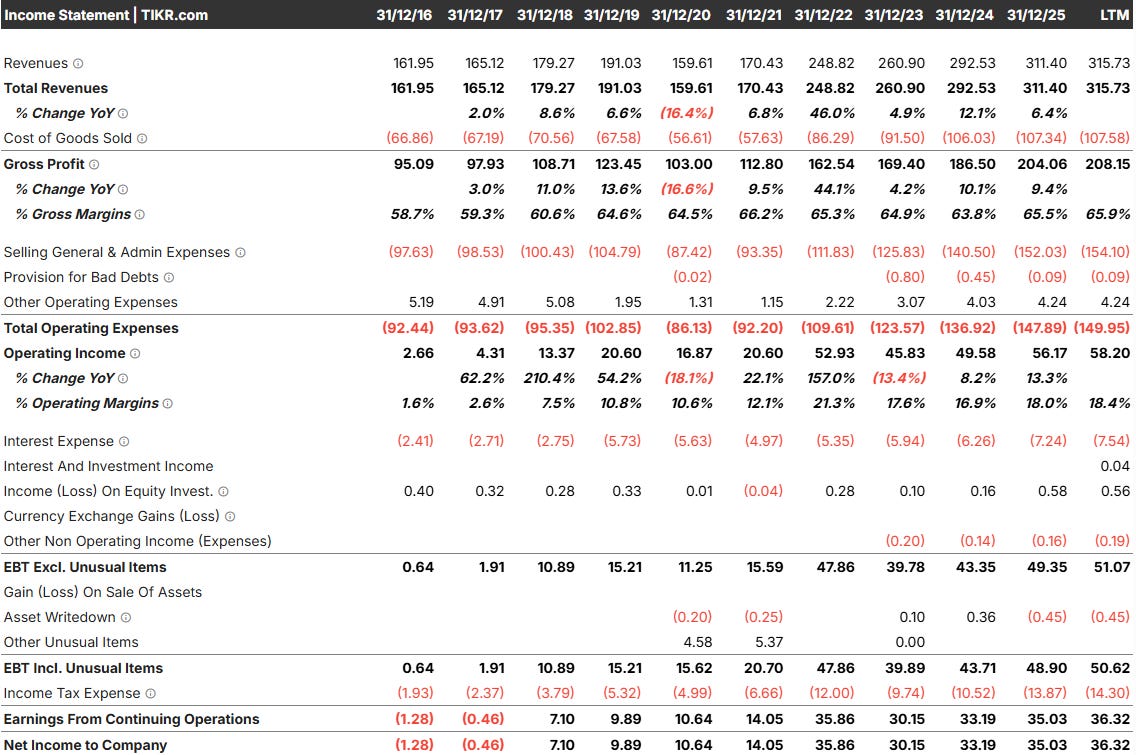

Where this idea gets really interesting is looking at the valuation. The company has been a consistent high single digits revenue grower and low double digits earnings grower as operating leverage has kicked in. Operating margins are a healthy 18%, while the company is running at a nice 20% return on capital, demonstrating that their store growth has been well executed so far. With all of this in mind, the valuation is astounding. At an MYR $332m market cap, the company has trailing 12 month earnings of around $37m putting them at a trailing PE of around 9. For a high quality, non-cyclical, low double digits earnings grower I think that this is much too cheap. On top of all of this, the company has a clear capital allocation strategy that is very shareholder friendly. At least 50% of net profit is paid out as a dividend each year (last year had a 60% payout ratio) with the rest being pushed mainly into new store openings. With the previously stated 20% ROIC, 20% margins for new stores at maturity, and a long runway for continued store openings I am very satisfied with their capital allocation, and the solid dividend means you don’t just have to rely on a rerating for a return here.

Risks and Why this Opportunity Exists

In these writeups I always love to answer the question “why does this opportunity exist”. Focus Point has my favourite answer to this question: nobody is looking. This is an illiquid, $83m USD microcap listed on the Malaysian stock exchange. There are no large substack writeups, next to no tweets about it and it’s too illiquid for any institutional money to play in. The free float is only around 25% with the majority of the shares being held by the founding family, or government and pension linked institutions.

As far as the actual risks, part of what attracts me to this situation is the lack of visible downside. The main risk would be a slowdown in growth and a decline in return from new stores. However, with only 20% penetration and a clear competitive edge I see them having a clear growth runway going forward. Obviously the company is somewhat exposed to the broader Malaysian economy, but as stated earlier the optical business is somewhat non-cyclical. The most likely risk to eventuate is continued underperformance in the F&B business, which could continue to be a drag on earnings. The most recent quarterly data suggests that this segment is going the other way, but it’s a low quality, consumer exposed business so could turn easily. Realistically though, it’s hard to see such a small segment being a significant drag on earnings long term, as opposed to just a minor speedbump.

One other risk here is the move to online Ecommerce that has hurt physical retailers globally. However, optical stores are uniquely positioned to deal with Ecommerce due to the need for eye testing that goes along with buying glasses. This inherently forces most customers into the store as they get their eyes tested and buy new glasses simultaneously. Furthermore, Malaysia’s Medical Device Authority recently enacted a ban on online contact lens sales, which is a regulatory tailwind that will force many customers who may have transitioned to online back to physical sales.

Conclusion

Focus Point is as clean a pitch as it gets in small cap emerging markets, with a dominant market position, non-cyclical demand, decade of consistent execution, founder alignment, and a clear reinvestment runway. At 9x trailing earnings with low double digit growth and a 50%+ dividend payout it’s hard to see how you lose a significant amount of money here outside of some sort of disaster. The fact is that nobody is looking at this little corner of the Malaysian exchange, resulting in what I believe to be a significant mispricing in a high quality microcap. Full disclosure I own a small position, limited by liquidity constraints.

Very interesting company, thanks Myles.

Fantastic! Thanks, I will look more closely.