Centurion Corporation

A Low Key Emerging Market Compounder

Before I start this writeup, followers of my Twitter and Substack will notice that I seem to have an affinity with Singaporean stocks. A disproportionate amount of my portfolio and stock commentary has been focused on Singapore which seems weird for someone based in Australia and I figured it was worth an explanation. The Singaporean exchange is a pretty poor exchange all together. It’s laden with low quality value traps with economic and geopolitical risk, along with generally terrible corporate governance. Additionally the exchange is very illiquid, and stocks are hard to move in and out of. However, that’s where the opportunity lies in my opinion. Other English reporting countries such as Australia, US and Canada are followed by many talented microcap investors who cover essentially the whole exchanges in detail, reducing the chance of “no brainer” ideas. The less popular exchanges such as the Chinese, Japanese and various European exchanges pose a language barrier to me that can be very frustrating. The SGX doesn’t have these issues. Due to the general low quality and illiquidity it’s just not worth it for a lot of investors to look at, meanwhile all of their filings are in good old English. Naturally, that makes it a very attractive exchange for someone without liquidity constraints that’s willing to put in the time to find diamonds in the rough.

With that out of the way I want to introduce you all to Centurion Corporation ($OU8), a Singapore based worker and student housing provider. Their student housing services are based out of mainly the UK, with some exposure to Australia and the US and accounts for around a quarter of their revenue. Meanwhile their worker accommodation operations are based mainly in Singapore with some Malaysian exposure and accounts for the other 3 quarters of revenue. The company operates in an interesting niche that is experiencing a large amount of growth, with demand for student housing and worker accommodation surging in the years since the pandemic.

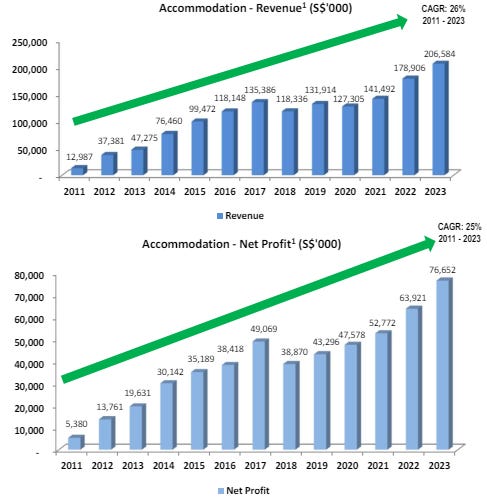

The company has a pretty impressive track record for a cheap, emerging market small cap. The company operated as a CD and DVD manufacturer for decades before making an incredible pivot into student and worker housing in 2010, steadily phasing the manufacturing out over the 2010’s. Since then the company has grown profitably at around a 25% CAGR for both revenues and profits, while the total return for shareholders has been 400%. The company is a proven operator with a model that clearly works.

The core question is the sustainability of earnings. After being suppressed due to travel restrictions during covid, both worker and student accommodation has been in high demand globally as international workers and immigrants have flooded back into developed nations. Occupancy rates are very high, while rents remain quite strong across the portfolio. Meanwhile, supply hasn’t been able to keep up due to delays initially due to Covid, and now due to labour issues and materials prices. Long term Management has been very bullish with their rhetoric, asserting in presentations that this is long term, secular demand growth as opposed to a temporary cyclical high and I’m inclined to agree, especially as it comes to the UK, US and Australian markets which I know better. Centurion is well positioned to take advantage of that demand with an experienced management team and a proven growth strategy. They currently expect worker accommodation beds to increase by 7% and student housing beds to increase by 1% in 2024 based on projects currently in the pipeline, with further growth planned onwards. Currently Centurion is being priced as a low quality, cyclical shitco, however I believe it may be a decent quality business in a growing niche with a high quality management team.

Centurion truly is trading like a cyclical shitco. Annualising their second half underlying profit gets us to $70m of profit for the year, around 8 cents a share on a share price of 50 cents for a PE of just over 6. Once backing out non cash items their cash flow conversion is strong. Their balance sheet isn’t fantastic with $600m in net debt, however their average maturity date is 6 years with maturities fairly spread out and the carrying value of their investment properties and joint venture is $1.54B, leaving them fairly well covered. Additionally, their margins are strong, with 40% operating margins leaving them resilient to potential revenue weakness were the cycle to turn. Revenue would need to halve (with no change in costs) for the company to make an operating loss. The company has announced a final dividend of 1.5 cent a share, bringing their full year dividend to 2.5 cents, or a 5% yield. As an emerging market small cap this brings me comfort, as we aren’t just relying on a rerating of the stock to do well here, and could feasibly do well through a steadily growing dividend yield.

One thing that really attracts me in this situation is management. Most of the management team have been around for 10 or more years, a period in which they’ve pulled off an incredible transition from crappy manufacturer into a well run real estate business. Their results over the past decade speak for themselves. The management team are all incredibly aligned, with the Joint Chairmen owning 50% of the company between the two of them and the Deputy Chairman and COO both owning more than $5m of stock. Obviously with this comes risk as minority shareholders will just be along with the ride, but management have done nothing to elicit concern about poor governance or behaviour. As a bonus, what brought this stock onto my radar initially was the slew of not insubstantial purchases by management earlier this year. It’s nice to know management still finds the stock attractive and are putting their money where their mouths are.

In Centurion Corp I believe we are being presented with an opportunity to purchase a decent quality company with a good management team at a bargain basement price. While there may be cyclical risks in the medium term as more supply comes online, the short term outlook is strong while I expect them to continue to grow earnings over the longer term as they have over the past decade. I could see multibagger potential through a combination of earnings growth and an improved multiple as they continue to execute. I currently have around a 5% position and may even add trim some other positions to add more.

Looks like revenues per bed have gone up significantly since 2019, up 50% or so. A bit odd, no?

"The company has announced a final dividend of 1.5 cent a share, bringing their full year dividend to 2.5 cents, or a 5% yield.

is there any witholding tax deducted and if, how many % ?